Worldwide spending on information and communications technology (ICT) reached nearly $4,7-trillion in 2022 and, after a slightly slower 2023, is forecast to grow steadily through 2027 with a 5,7% compound annual growth rate (CAGR), according to the latest update to the International Data Corporation (IDC) Worldwide ICT Spending Guide: Enterprise and SMB by Industry.

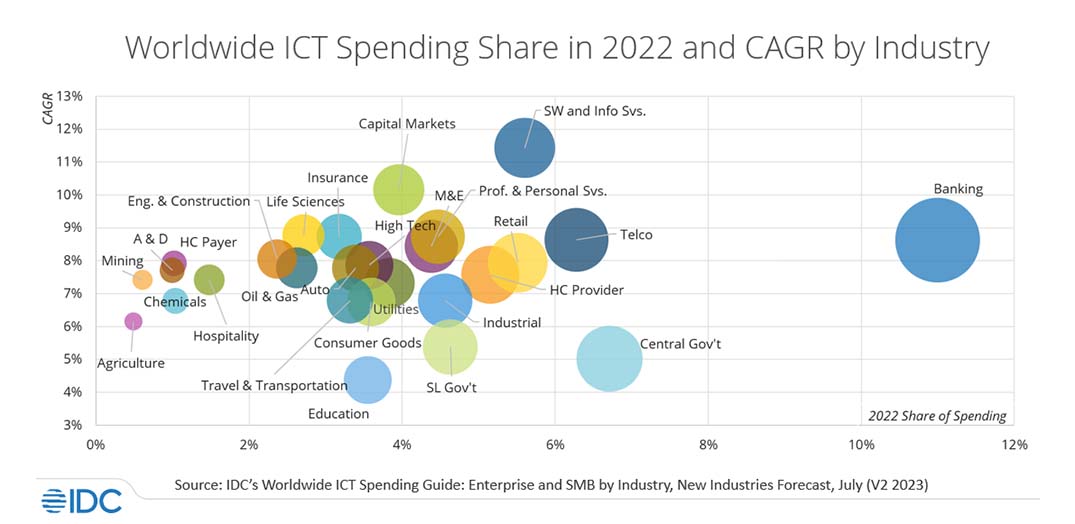

Despite a slowdown across various segments of this industry in the past year and recent layoffs, Software and Information Services will be the fastest growing industry over the 2023-2027 forecast period, generating an 11,4% CAGR as technology companies have engaged in some course correction initiatives after rapid expansion in investments and hiring seen in previous years. Capital Markets will be the second fastest growing industry with a CAGR of 10,2% followed by the Life Sciences industry with an 8,8% CAGR, partially driven by growth in China.

The three industries (excluding Consumer) with the largest ICT investments in 2022 were Banking, Federal/Central Government, and Telecommunications. Together, these industries generated $715-billion in ICT spending worldwide. Software and Information Services and Retail were the next largest industries in terms of ICT spending in 2022, giving the top five industries a combined share of overall spending of nearly 35%.

From a technology perspective, growth will be driven by Software with a 12% CAGR, driven by investments in Enterprise Resource Management Applications, Content Workflow and Management Applications, and Security Software.

The fastest growing technologies within the Software category include Artificial Intelligence Applications (36.3% CAGR) and Integration and Orchestration Middleware (22,1% CAGR). Hardware and Telecom Services will be the two largest areas of ICT spending, but also the slowest growing with CAGRs of 4,2% and 2,6% respectively. Business Services and IT Services will see growth near the overall market average.

The US will be the largest geographic market in terms of ICT spending, forecast to reach $2,38-trillion in 2027. Western Europe will be the second largest market in 2027 with investments totaling $1,19-trillion, followed by China at $721-billion. Latin America will see the fastest spending growth with a five-year CAGR of 8%, followed by US and China.

This version of the Spending Guide utilises IDC’s new industry taxonomy, described in the recently published study, IDC’s New Industry Framework, Definitions, and Transition Plan. The taxonomy update brings deeper analysis capabilities to market through enhanced visibility into sectors, sub-sectors (sector detail level), and industries, increasing the total number of industries covered from 20 to 28. The expansion was developed in response to customer demand and created by researching existing industry taxonomies, including economic standards, client inquiries, technology vendor target industries, and competitive taxonomies.

“The introduction of the new IDC Industry taxonomy marks a significant leap forward in our ability to support our clients’ industry segmentation needs. With more modern categorization and granular, value chain-based segmentation, IDC data users are better equipped to identify, analyze, validate, and action questions and insights specific to the industries they serve,” says Eileen Smith, program vice-president: data and analytics at IDC.

“Analysts and strategists can track trends across more industries, validating assumptions while understanding nuances of buyer behavior and whether these change in adjacent segments. Executives and their teams can better inform strategic decisions and justify tactical actions, such as acquisitions, partner selection, resource allocation, and territory and campaign planning at granular industry levels.”