Global spending on information and communications technology (ICT) is forecast to reach $4-trillion in 2026 and surpass $6-trillion by 2029, according to the latest update of the International Data Corporation’s (IDC) Worldwide ICT Spending Guide Enterprise and SMB by Industry.

Excluding the consumer segment, the ICT market is projected to grow 10% in 2026, driven by rapid adoption of Artificial Intelligence (AI) platforms, which will grow over 70% by the end of the year.

Main technology drivers for ICT spending

Software emerges as the largest technology group in 2026, absorbing more than 33% of global ICT spending. This surge is primarily fueled by robust investments in enterprise resource management (ERM) applications, security software, and production and operations applications, which together will account for over one-third of total global software expenditure.

These categories reflect enterprises’ ongoing priorities around operational efficiency and cybersecurity resilience.

Hardware is set to be the fastest growing technology group, with a projected year-over-year growth rate of 15% in 2026. This expansion is driven by significant momentum in non-x86 servers, the proliferation of wearables, and increased adoption of Infrastructure-as-a-Service (IaaS). T

his underscores the rising demand for specialised compute infrastructure, edge devices, and scalable cloud resources to support next-generation workloads and hybrid environments.

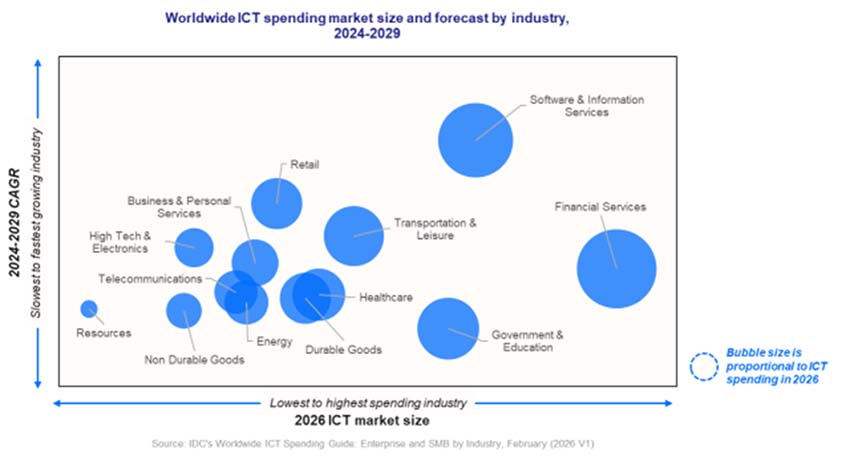

Global ICT market at a glance

- Total ICT spending: $4-trillion (+10% YoY)

- Software: Largest tech group at more than 33% of spend

- Hardware: Fastest growth at more than 15% YoY

- Top industries: Software and Information Services, Banking, Retail (more than $1-trillion combined)

- Fastest-growing sectors: Software and Information Services, Media and Entertainment, Retail

- Leading regions: US ($2-trillion), Western Europe ($908-billion), China ($355-billion)

- Five-year CAGR more than 10%: US, China, Latin America

“We are entering a new phase of the AI-everywhere journey: the era of expectations and reckoning,” says Andrea Siviero, senior director at IDC. “The excitement of experimentation is giving way to a sharper focus on accountability, value creation, and productivity impact.

“In 2026, enterprises will demand that AI and digital investments demonstrably improve processes, accelerate decision making, and ultimately drive business growth across the organisation.”

Key global dynamics

Major global events in 2025, including escalating trade tariffs, security threats, and the US government shutdowns, prompted organisations to accelerate investments in AI-driven optimization and security.

Geopolitical tensions and supply chain disruptions accelerated digital transformation and security spending.

The US will lead global ICT spending in 2026, reaching $2-trillion, driven by its large enterprise base and rapid adoption of cloud and AI technologies.

Western Europe will be the second largest market at $908-billion, supported by regulatory-driven modernisation and accelerated AI adoption in sectors like banking and manufacturing.

China will follow with $355-billion, fueled by government-led digital infrastructure and expansion of smart manufacturing and AI platforms.

Key industry trends in ICT spending?

Software and information services, banking, and retail will be the three largest spending industries and together will represent over $1-billion in ICT spending in 2026.

The next five largest industries – federal/central government, telecommunications, media and entertainment, healthcare provider, and high tech and electronics – will together account for more than 20% of worldwide spending.

“As companies continue to invest in automation, industries such as aerospace and defense, insurance, and software and information services are poised to accelerate spending in AI platforms the fastest,” says Andrea Minonne, research manager at IDC.

“In aerospace and defense, escalating geopolitical cross-regional tensions and heightened security concerns are prompting governments to expand defense budgets.”

Looking at other fast-growing vertical markets, insurance firms are leveraging AI platforms to manage rising claims volumes, improve risk modelling, and deliver real-time health insights, responding to both regulatory demands and evolving customer expectations.

Software and information services are at the forefront of deploying generative and agentic AI to automate business processes, enable intelligent workflow orchestration, and support scalable digital transformation initiatives.

Meanwhile, high tech and electronics, automotive, and consumer goods are navigating ongoing frictions including trade tariffs and talent shortages and are prioritizing nearshoring strategies, factory automation, and advanced analytics.

These investments are enabling organizations to mitigate supply chain risks, optimise production, and maintain competitiveness in a volatile global market.

Software and information services, banking, and retail will be the three largest spending industries and together will represent over $1-billion in ICT spending in 2026. The next five largest industries will account for more than 20% of worldwide spending.