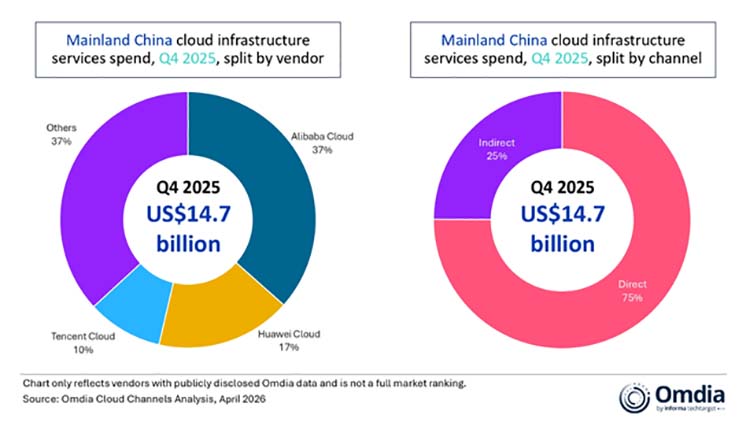

Mainland China’s cloud infrastructure services spending reached $14,7-billion in Q4 2025, up 26% year-on-year, according to new research by Omdia.

This marked a continued acceleration from the previous quarter and the third consecutive quarter of growth above 20%.

Looking ahead, Omdia forecasts that China’s cloud infrastructure services spending will grow by 26% in 2026.

In Q4 2025, AI remained the market’s primary growth driver, but its impact expanded beyond model-related demand to support broader cloud infrastructure consumption and enterprise deployment capabilities.

At the same time, market attention is shifting from models themselves toward product forms such as agents that are more closely aligned with real-world business processes.

Competition is increasingly centered on product readiness, operational capability, and the depth of scenario integration. As AI adoption moves closer to real business workflows, collaboration across the broader ecosystem is also set to play a more important role.

Mainland China’s cloud infrastructure services market continued to recover in Q4 2025, posting 26% year-on-year growth. AI-related demand remained the central growth driver. As enterprise AI adoption deepened, market growth was increasingly supported not only by model usage, but also by the broader rollout of enterprise AI, the expansion of private AI deployments, and rising demand for traditional cloud resources such as compute, storage, and databases.

“This reflects a broader shift in the role of AI, from a standalone technical capability into a wider driver of infrastructure demand,” says Rachel Brindley, senior research director at Omdia. “As enterprises embed AI across a wider range of real-world business scenarios, deployment models, data environments, and operational frameworks are becoming increasingly complex.

“As a result, demand for cloud resources is extending beyond model consumption to the broader infrastructure layer.”

AI commercialisation is also gradually evolving beyond chatbot-style applications toward execution-oriented applications, particularly agents.

The rapid emergence of OpenClaw in China has further heightened market attention on this shift. More importantly, it has given the market a clearer view of how agents can connect workflows, tool use, and external systems through conversational interfaces, while being packaged into product forms that are more closely aligned with business process.

“As conversational interfaces, workflows, and enterprise systems are increasingly integrated into the invocation and execution chain of agents, the focus of market competition is beginning to shift,” says Yi Zhang, senior analyst at Omdia. “It is moving beyond models and platform capabilities alone toward the deliverability and operational maturity of agent products, as well as the depth of their integration with real-world business scenarios.”

As this shift becomes more visible, China’s leading cloud vendors are responding in different ways, with each placing emphasis on different parts of the emerging agent landscape.

Tencent Cloud is emphasising the value of the interface layer, accelerating its agent product strategy around mainstream instant messaging platforms and its broader ecosystem, while exploring how messaging and chat interfaces can evolve into points of invocation and execution for agents.

Alibaba Cloud is placing greater emphasis on the enterprise platform layer, strengthening enterprise-grade agent platforms and workflow execution capabilities to support agent adoption across business processes.

Huawei Cloud, meanwhile, continues to advance AI deployment through industry scenarios, with a stronger emphasis on the integrated development of models, platforms, and solution capabilities.

As agents move closer to real business processes, ecosystem collaboration is becoming more important. In Q4 2025, partner-driven cloud revenue accounted for 25% of the market, with the share expected to rise further as partners help translate AI adoption into business value.